Article by Joachim Klement, Investment Strategist at Panmure Liberum

The average actively managed fund underperforms the market, as we know. But how does the average fund manager squander the performance? Is it by picking the wrong stocks or by investing in the right stocks but at the wrong time?

Javier Vidal-Garcia and Marta Vidal tried to find out by decomposing the returns of more than 21,000 active equity funds investing in 35 different countries between 1990 and 2025. Because they only looked at single-country funds rather than regional or global funds, the total assets under management of these funds were just over $12bn (country funds remain a niche endeavour in most countries).

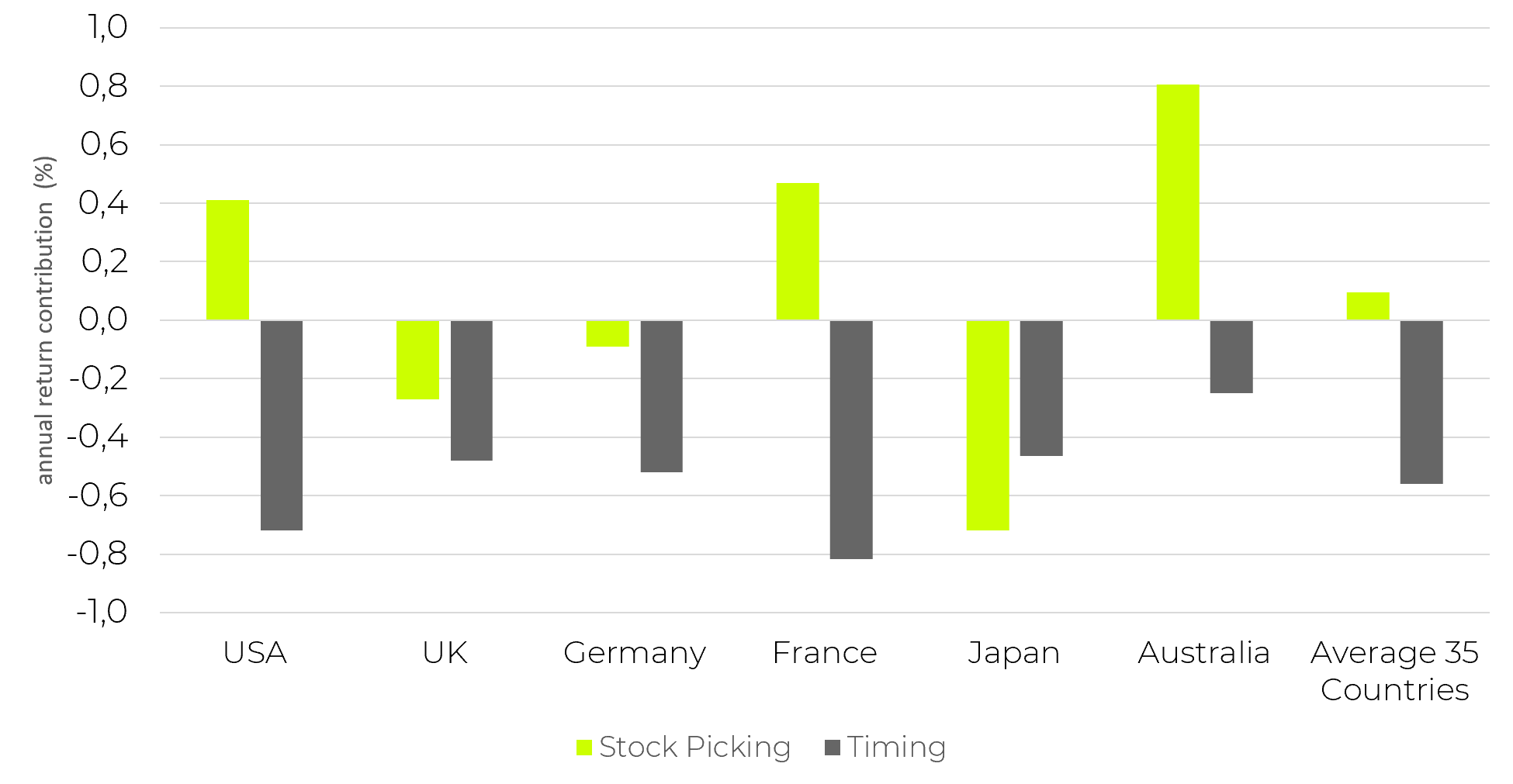

The chart below displays the results of this return decomposition for funds in selected countries, compared to the total market performance in each respective country. As you can see, the primary driver of underperformance is the timing of stock purchases and sales, rather than stock picking itself. In every one of the 35 markets studied, fund managers, on average, lost performance due to their market timing activities. The drag from market timing was an average 0.43% per year. Meanwhile, stock picking contributed positively in some countries and negatively in others. Still, there was no clear trend, and the average of the 35 countries tested was slightly positive at 0.09% per year.

Source: Vidal-Garcia and Vidal (2025)

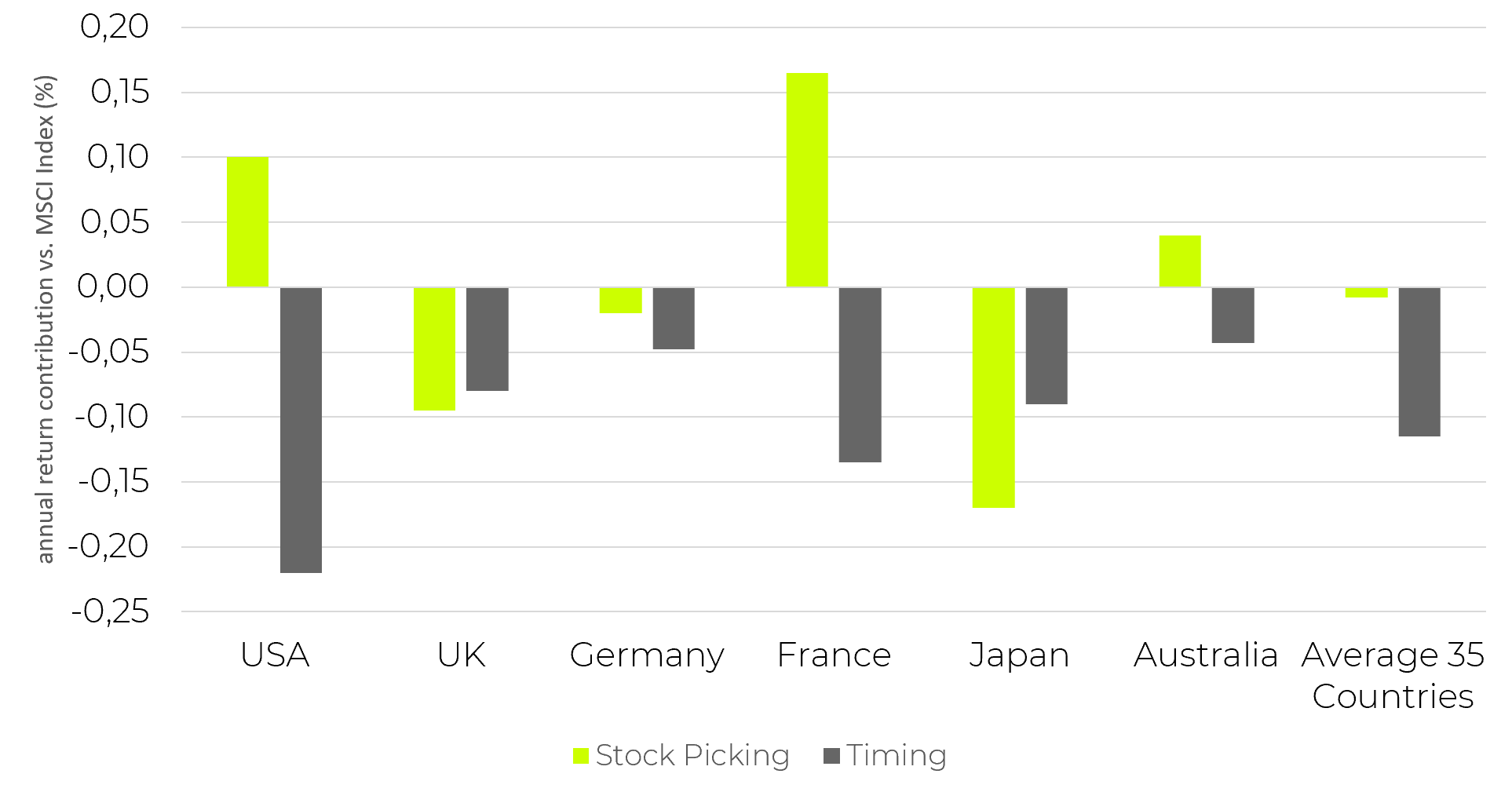

But this is not the whole story. Most funds are managed against a benchmark that is more restricted than the market overall. The typical benchmark is the MSCI index covering the respective country. So, they did the same decomposition for the MSCI country index vs. the total market.

In the chart below, I calculated the difference between the average fund manager and the MSCI country index to determine where fund managers underperform compared to a typical benchmark index, rather than the market.

Source: Vidal-Garcia and Vidal (2025)

As you can see, market timing is still the primary driver of underperformance. Indeed, on average across 35 countries, it is the only driver of underperformance. Stock picking, meanwhile, is sometimes positive and sometimes negative, but on average does neither detract nor add to the performance of a fund vs. the MSCI.

The results are not great for active fund managers since the stock pickers, on average, aren’t able to add value through stock picking (though some obviously can). However, it suggests that fund managers seeking to enhance their performance may want to concentrate more on refining their market timing decisions rather than selecting the right stocks. This analysis suggests that there is more ‘alpha’ to be found by refining the investment process around timing decisions rather than stock selection decisions.