In brief: “Buy the Dip” sounds logical. But in a systematic form it has historically delivered weaker risk‑adjusted results than simply staying invested (buy and hold). AQR tests 196 variants – and finds robust timing “alpha” only rarely. Those who buy dips often end up, unintentionally, positioned against trend and momentum.

A reflex with a good reputation

When prices fall, the mood shifts quickly. Portfolios turn red, headlines get louder – and suddenly buying more sounds like the only sensible move. “Buy the dip” is the stock‑market formula for that moment. It promises that courage will be rewarded.

But courage in markets is not a method. And a good feeling is not evidence. AQR therefore treats dip buying not as a slogan, but as a strategy question: can it be turned into a rule that works reliably over many decades?

The answer is sobering – and precisely for that reason, useful.

What AQR actually tests – and why it matters

The phrase “buy the dip” sounds unambiguous. In practice, it is not. How deep does a dip have to be? Over what time window do you measure it? And how long do you hold the position afterwards? Without answers to these questions, you are not following a strategy – you are following a mood.

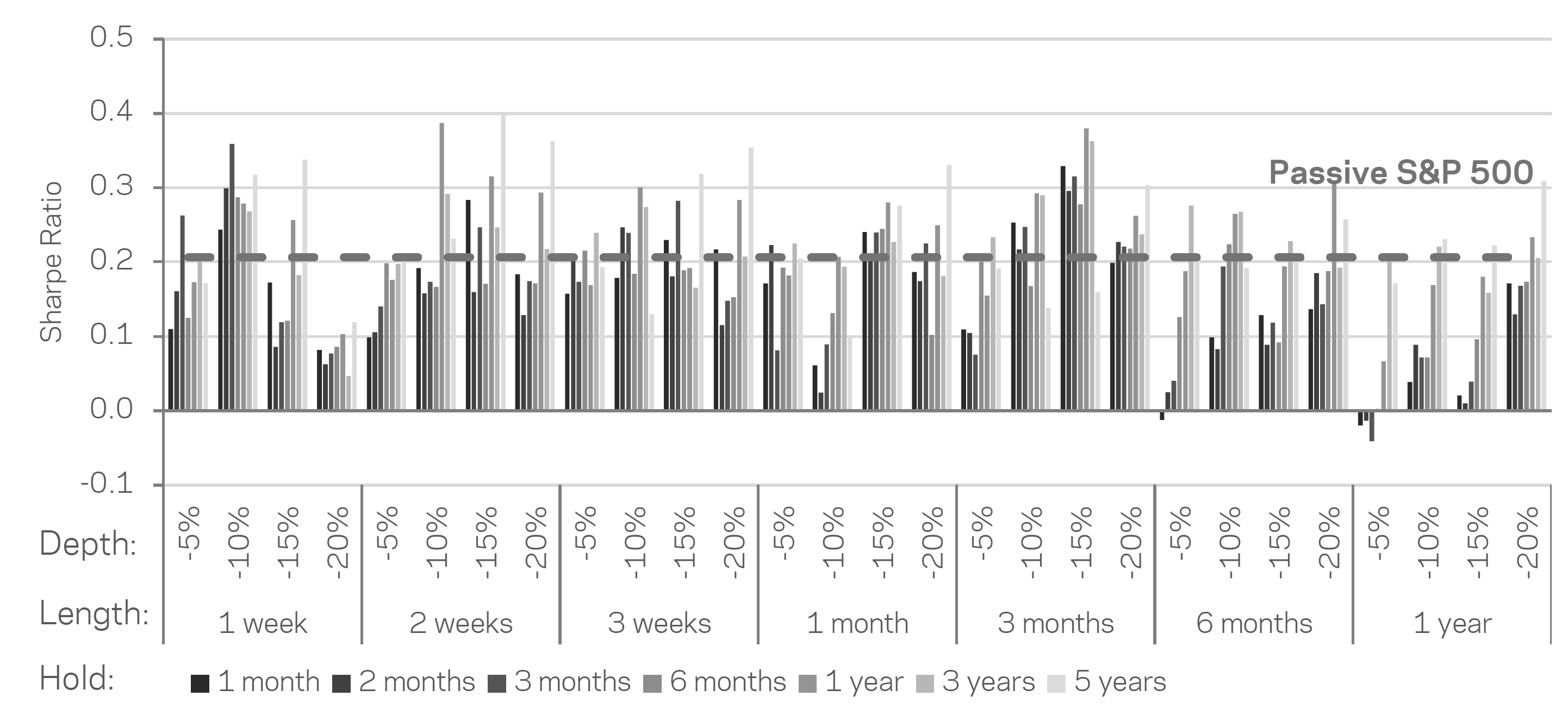

AQR turns the gut feeling into a toolkit. Three parameters are varied: the depth of the decline (–5% to –20%), the length (one week to one year) and the holding period after the purchase (one month to five years). This produces 196 different rules.

Important: in this construction, the strategy is otherwise in cash. It invests only when the “dip” rule is triggered. That is strict – and therefore a fair test for anyone who likes to “wait for the pullback.”

The core problem: those who wait are often not in the market

The mechanics already explains part of the result. Buy‑and‑hold is always invested and thus earns – through all fluctuations – the equity risk premium. A dip rule, by contrast, often sits on the sidelines and waits for a signal. Waiting can be sensible. But in markets it has a price: missed time in the market.

AQR puts it plainly: a strategy that is frequently in cash will struggle to beat a continuously invested portfolio – even if some entries look good.

The numbers: most variants do not beat buy‑and‑hold

AQR compares all 196 rules with passively holding the S&P 500. What matters is not only return, but risk‑adjusted return (Sharpe ratio). That is the standard yardstick if you want to judge timing strategies fairly.

The next picture is clear: on average, buy‑the‑dip variants sit below buy‑and‑hold. More than 60% of the rules underperform on a risk‑adjusted basis. Using more recent data (including dividend history), the gap becomes even larger.

And the promised “alpha”?

This is where it gets interesting. Many defend “buy the dip” not with averages, but with exceptions: “In the 2020 crisis it was great.” Or: “In 2022 it paid off.” These stories may be true. But they do not settle the strategy debate.

AQR therefore estimates alpha relative to passive equity exposure. On average, the result is a small positive alpha. But when you look at the statistics, hope fades: only a small fraction of the 196 variants reaches conventional significance. If you test 196 rules, a few “hits” are to be expected purely by chance. That is the data‑mining trap: you find a rule that looked good in the past – and mistake luck for robustness.

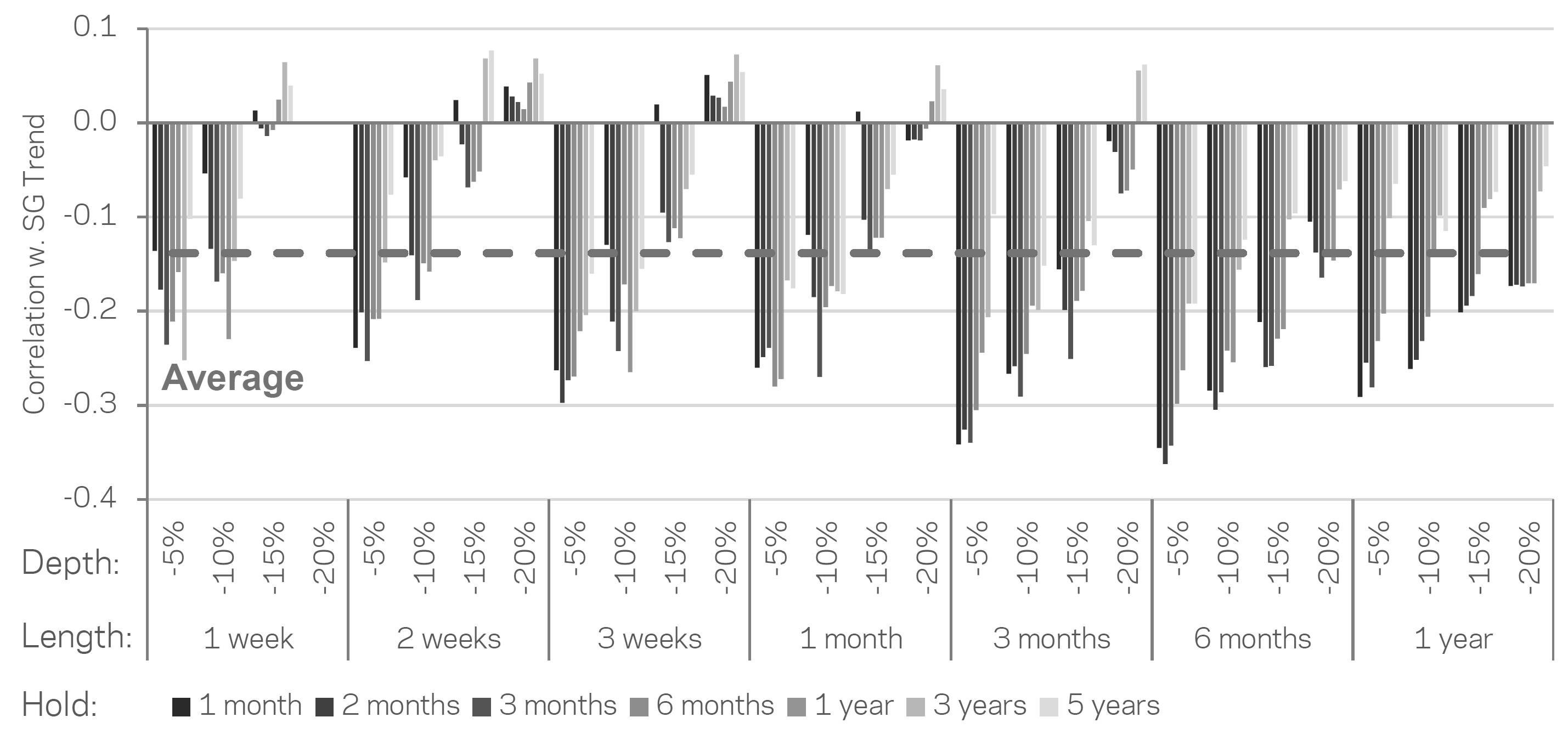

The blind spot: dip buying is often anti‑trend

The best part of AQR’s text is not the table, but the explanation. Buy‑the‑dip is often a reversal bet: it has fallen, so it must rise again. But markets can fall longer than a good slogan lasts.

AQR therefore compares buy‑the‑dip with a trend approach (proxy: SG Trend Index). In this comparison, trend following appears more efficient on a risk‑adjusted basis. And: dip strategies are, on average, negatively correlated with trend. Those who buy dips often end up on the other side of what works in many phases: the trend itself.

What one can take away

First: anyone investing for the long term should be cautious with rules that do one thing above all – reduce time invested. The most important return driver is often not the perfect entry point, but consistent participation.

Second: anyone who still wants to work tactically needs rules that do not just sound good, but rest on a clear economic rationale. And one has to accept that this rationale must hold across market regimes – not only in one’s favourite years.

Third: the psychological appeal of “buy the dip” remains. It is human. That is precisely why it pays to build a counterweight into the process: fixed rebalancing rules, a clear investment plan and a willingness to test simple stories against data.

In closing

“Buy the dip” is not wrong per se. It is just rarely as reliable as it sounds. AQR’s contribution is a useful reminder: in markets the question is not whether an idea feels intuitive, but whether it is repeatable – with rules that still hold when the next crisis looks different from the last.