THE SHARPE RATIO

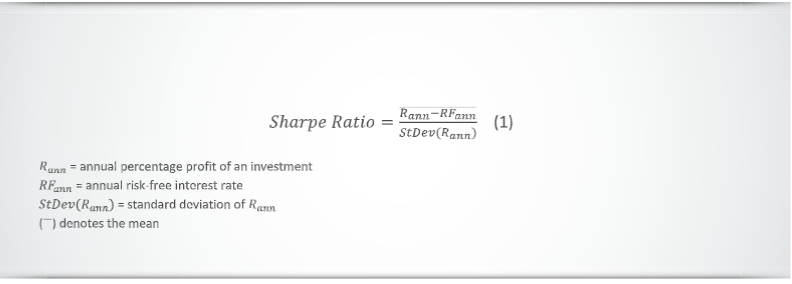

Originated in 1966 by William F. Sharpe as a performance gauge for mutual funds the Sharpe Ratio is nowadays the industry standard for the evaluation and optimization of investments and trading systems. The formula is the excess return in relation to the standard deviation and describes the reward/risk of the underlying investment:

Calculation EXAMPLE:

If an investment has an average annual profit of 10%,

the annual risk-free interest rate is at 2% and

the standard deviation of annual profits is 5%

Sharpe Ratio = (10% - 2%) / 5% = 1.6

The higher the Sharpe Ratio the better the Reward/Risk for the investment.

NO DISTINCTION BETWEEN GOOD AND BAD VOL ATILITY

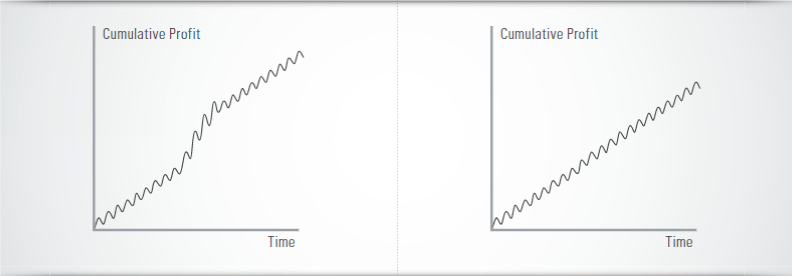

No matter how useful this formula is – there is a strong popular objection to the Sharpe Ratio as a global mean to gauge the risk-adjusted profitability of a trading system. The central point of this objection regards the use of standard deviation of all returns in the determination of risk: Using both positive and negative returns in the determination of risk, the Sharpe Ratio doesn’t separate “good” from “bad” volatility in performance although volatility which is generated by upward thrusts of the system’s profit curve is intuitively welcomed in contrast to volatility generated by downward thrusts of the curve. As shown in figure 1, the left profit curve, for example, is seen as riskier than the right one according to the way the Sharpe Ratio perceives risk although intuitively the left curve is much more appealing.

The Sharpe Ratio perceives risk as unpredictability of future performance not as possibility of losing money. Consequently, the left equity curve is seen as more risky by the Sharpe Ratio than the right one.

As a more sophisticated example, the Sharpe Ratio might see the same risk in a trend following type of system (which has many small loosing trades and a few amazingly profitable ones) and in a system which systematically shorts uncovered options thus having many small profitable trades and a few very large losses. The distribution of profits of the first system is usually positively skewed¹ whereas the second system has usually a negatively skewed distribution (see figure 2).

But perhaps in the second system there may be much more hidden risk of losing capital due to the possibility of black swan events (sudden extremely rare unfavorable situation for the system).

The Sharpe Ratio defines risk as deviation of returns above or below their mean

It appraises positively and negatively skewed distribution of returns the same way with respect to risk

¹ skewness is a measure of asymmetry for a distribution.

The Sharpe Ratio appraises positive and negative skews the same way.

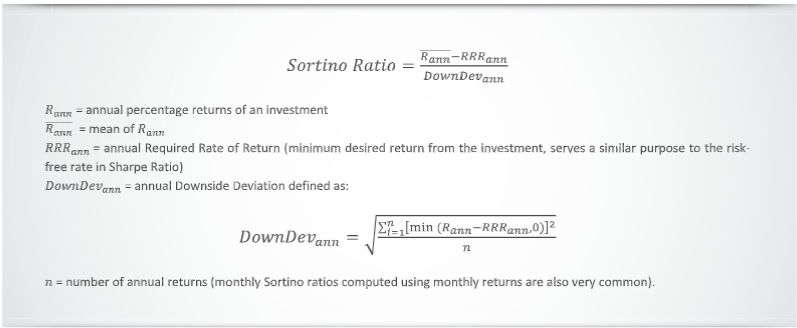

THE SORTINO RATIO – DOWNWARD VOLATILITY DEFINES THE RISK

An alternative Reward / Risk metric to the Sharpe Ratio is the Sortino Ratio which separates upward volatility from downward one and it uses the latter to represent the system‘s risk. The Sortino Ratio was created by Brian M. Rom in 1983 and it derives its name from Frank Sortino who advocated the use of only downside deviation from a desired minimum return as a proxy of risk. The typical discrete formula version of the annual Sortino Ratio commonly used is: